What will change with the new lease accounting standards? Impact of the revisions and key points for practical implementation.

HULFT 's problem-solving solutions | For accounting and finance departments

The new lease accounting standards are a system revision that will be applied from April 1, 2027, and will revise the accounting treatment of lease transactions.

This amendment could potentially change the figures in the financial statements of many companies, and is also expected to affect how accounting operations are conducted.

What are the new lease accounting standards?

Companies utilize various assets, such as office leases, office equipment, and manufacturing facilities, through lease agreements.

Under conventional accounting standards, these rents were treated as monthly expenses and were not recorded as assets or liabilities on the balance sheet.

In reality, there was a significant amount of lease usage, but this was not adequately reflected in the financial statements. This is what is known as an "off-balance sheet" situation.

The new lease accounting standards are being introduced to rectify this situation.

In simple terms, the new lease accounting standard requires that assets used under lease be recorded on the balance sheet as assets and liabilities, rather than simply as "borrowed items." This makes the actual usage, which was previously not reflected in financial statements, visible in numerical terms, thereby increasing the transparency of the financial situation.

On the other hand, while the inclusion of leased assets increases "total assets" and "total liabilities," the amount of equity remains unchanged. Therefore, the "equity ratio," calculated as equity divided by total assets, may relatively decrease.

Furthermore, since it is necessary to calculate the depreciation of the right-of-use asset and the interest on the lease liability for each lease agreement, there are concerns that this will significantly increase the practical burden on the finance and accounting department.

Thus, the new lease accounting standards are not merely a change in processing methods, but rather a systemic reform that will have a significant impact on how financial statements are presented and on daily accounting operations.

Impact on businesses and practical challenges

Adapting to the new lease accounting standards involves far more practical work than one might anticipate. It's not simply a matter of changing journal entries; the scope of work is extensive, encompassing everything from policy formulation and contract management to calculations and ongoing operation.

The main points to address, organized according to the practical workflow, are as follows:

| Corresponding items | Main contents |

|---|---|

| Collection and understanding of contract information | We collected all contracts scattered across all locations and departments and organized the contract period, renewal clauses, payment terms, etc. |

| Determining whether something qualifies as a lease | Determine whether each contract qualifies as a lease subject to the new lease accounting standards. |

| Present Value Calculation and Accounting | Estimating future lease payments, setting discount rates, calculating present value, and accounting for right-of-use assets and lease liabilities. |

| Re-estimate due to changes in contract terms | If there are any changes to the contract period or rent, assets and liabilities will be recalculated. |

| Grouping support | For companies with multiple locations, contracts are grouped and calculated for each cash flow generation unit. |

| Integration with accounting systems | Journal entry generation, fixed asset management, data integration and consistency with accounting systems. |

| Development of internal controls and information sharing | Building a system to ensure that information is reliably shared with accounting when contracts are signed or amended. |

These are not one-time issues. Ongoing processing is required with each financial settlement, and any contract changes necessitate recalculations.

For companies with a large number of contracts, the number can range from tens to hundreds, and sometimes even more. If these are managed manually or using Excel, risks such as input errors, calculation errors, missed updates, and inconsistencies in judgment are unavoidable.

Adapting to the new lease accounting standards presents a significant burden in terms of workload, frequency, accuracy, and control, making it a practical challenge where manual, reliant operations are likely to reach their limits.

Key points for preparing for and responding to the new lease accounting standards.

As discussed in the previous chapter, it is not realistic to continue managing these things solely by hand or using spreadsheet software.

The important thing is to create a system that does not make tasks dependent on individuals.

The first thing that's needed is a platform that allows for centralized management of contract information.

It is essential to have an environment where contract details, duration, payment terms, and renewal information can be centralized and kept up-to-date at all times. For companies with a large number of contracts, the dispersion of information and failure to update information pose a significant risk.

Next, a system that can automate the determination of lease eligibility, present value calculation, and depreciation calculation is crucial.

By pre-configuring discount rate settings and calculation logic, and creating an environment where accurate figures can be calculated each time a settlement is made, the workload and human error can be significantly reduced.

Furthermore, data integration with accounting systems and fixed asset management systems is essential.

Manually entering and transferring calculation results has limitations in both efficiency and control. Automating the integration of journal entry data would significantly improve the speed and accuracy of financial closing operations.

Furthermore, it is desirable to have a system in place that automatically updates the calculations when contract changes occur, by updating the conditions.

An operational design that takes into account continuously occurring processes is necessary.

Adapting to the new lease accounting standards is not a temporary regulatory change, but rather a long-term redesign of business processes.

Systematizing contract management and calculation processes, including data integration, is key to stable and efficient operation.

Efficient response model through system integration

Here, we introduce services that can be used to specifically implement the correspondence model described in the previous chapter.

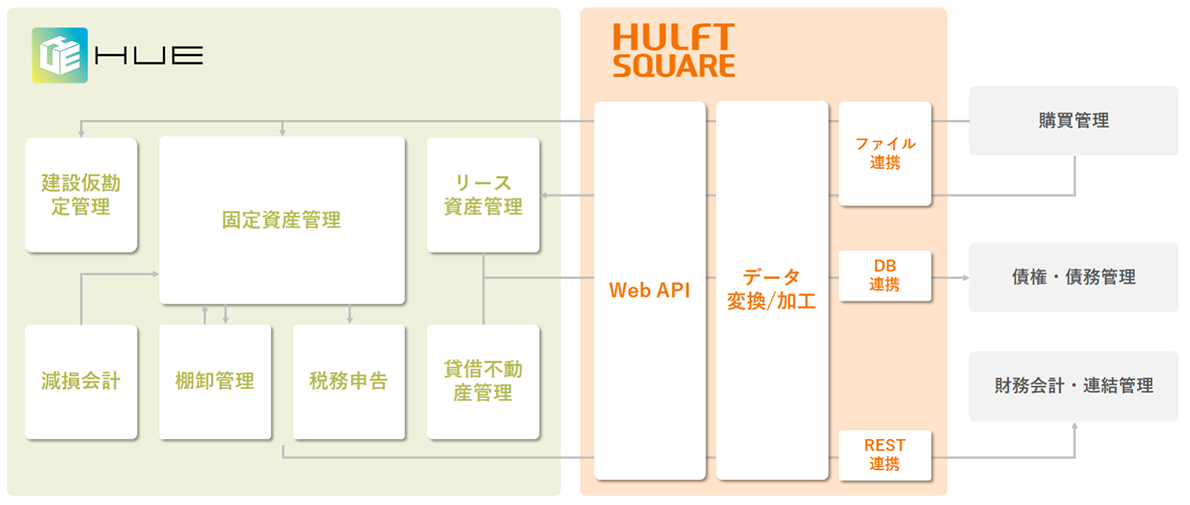

Adapting to the new lease accounting standards requires a fixed asset management system that handles centralized management and calculation of contract information, as well as a data integration mechanism that ensures reliable linkage of that data to various systems.

For example, by utilizing HUE, which handles the centralized management and accounting of lease agreements, and HULFT Square, which handles data integration between systems, it is possible to build a consistent workflow from contract management to calculation processing and data integration to accounting systems.

HUE is a domestically produced ERP system for large Japanese companies that offers unparalleled comprehensiveness of business processes, enabling them to effortlessly achieve a "Fit to Standard" solution even in the face of complex business requirements.

HULFT Square is a Japan-developed iPaaS (cloud-based data integration platform) that supports "data preparation for data utilization" and "data integration to connect business systems."

HULFT Square offers an application to facilitate seamless connection with HUE.

This allows for smooth data integration between other systems and HUE while minimizing the burden of setting up the integration.

This significantly reduces the burden of individual development and relay server construction, making it much easier to implement.

summary

As explained above, the application of the new lease accounting standards will change how figures are presented in financial statements, which may consequently affect management indicators.

In practice, a surprising amount of work is involved, from complex accounting processes to ensuring reliable integration with purchasing management and financial accounting systems. Moreover, these are not one-time occurrences, but processes that occur continuously with each accounting period. A manual approach would result in significant burdens and risks.

Given these circumstances, by using an asset management system to centrally manage contract information and perform accounting processing, and then reliably connecting the results to various systems using data integration solution, it becomes possible to smoothly implement regulatory compliance into operations.

Our company provides support for resolving various system integration challenges, including through our data integration platform, "HULFT Square."

We also offer consultations regarding implementation, including designing connections between the asset management system and surrounding systems, and building integration flows, tailored to your specific business needs.

- I would like to organize our overall policy for responding to the new lease accounting standards.

- We would like to consider how to integrate with each system.

- I'd like to discuss the specific steps involved in implementing this.

If you have any requests like these, please feel free to contact us.